ASOS

Read More about ASOSThe EU Carbon Border Adjustment Mechanism (CBAM)

The Carbon Border Adjustment Mechanism (CBAM) is an EU regulation that puts a carbon price on imports of certain carbon-intensive goods, including steel, aluminium, cement and fertilisers. Its definitive phase began on 1 January 2026, when EU importers bringing in more than 50 tonnes of covered goods a year became financially liable for the emissions embedded in those imports.

What is the Carbon Border Adjustment Mechanism (CBAM)?

The Carbon Border Adjustment Mechanism is the EU’s tool for putting a carbon price on imported goods, so that imports carry a cost similar to the one EU producers already pay under the EU Emissions Trading System (ETS). Its purpose is to prevent carbon leakage. Carbon leakage happens when production moves to countries with weaker climate rules, or when EU goods are undercut by cheaper, higher-emission imports. By pricing the emissions embedded in covered imports, CBAM is designed to level the playing field while encouraging cleaner production worldwide.

In short, CBAM turns the carbon emitted in making a product into a regulated cost at the EU border, rather than a voluntary sustainability metric.

Which goods are in scope of CBAM?

CBAM currently covers iron and steel, aluminium, cement, fertilisers, hydrogen, electricity, and selected precursors, chosen for carbon intensity and leakage risk. Once fully phased in, it’s expected to cover over half of EU ETS emissions.

The European Commission has proposed extending CBAM to downstream steel and aluminium products from 2028, not yet law, so worth tracking rather than assuming.

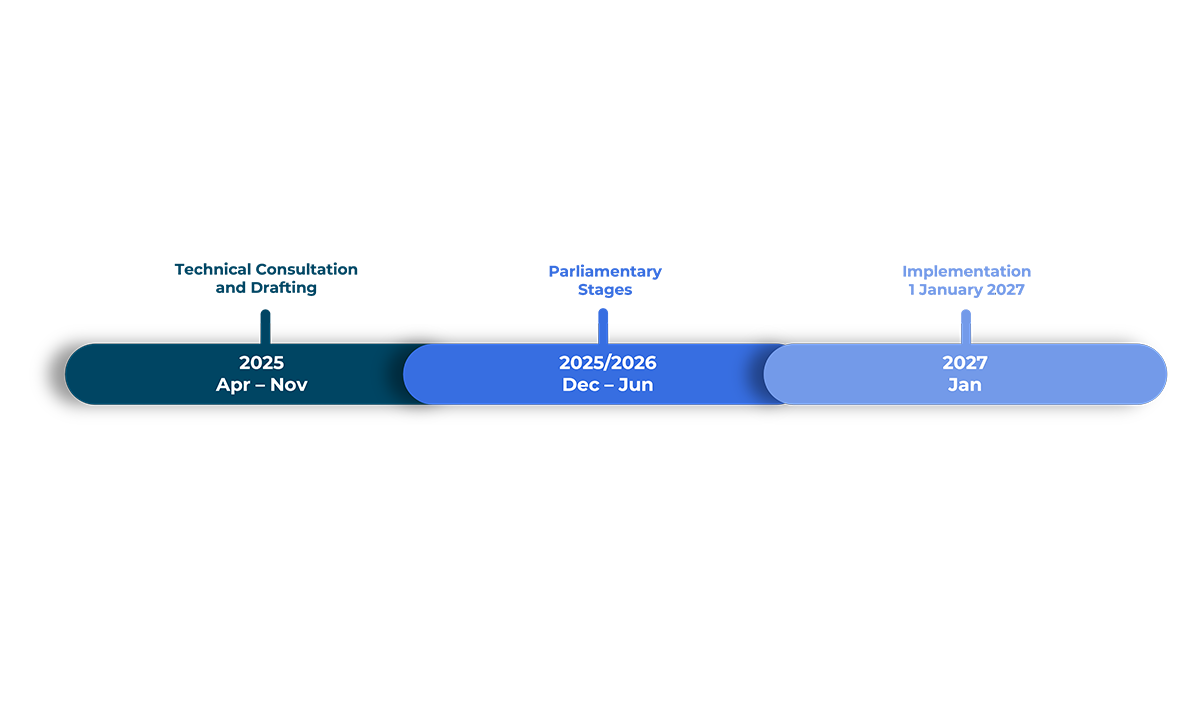

The CBAM timeline: transitional and definitive phases

CBAM has been introduced in two stages, and knowing which phase applies matters for what a business has to do.

The transitional phase ran from 1 October 2023 to the end of 2025. During this period, importers had to report the emissions embedded in covered goods each quarter, but there were no financial payments. It was a learning phase.

The definitive phase began on 1st January 2026. From that date, EU importers of covered goods became financially liable for the embedded emissions in their imports. Importantly, while liability applies to 2026 imports, the actual purchase and surrender of CBAM certificates does not begin until 2027, so the cost is real from 2026 even though the cash payment follows later.

Learn how the timeline impacts youAhead of the definitive phase, the EU adopted a set of targeted simplifications through the CBAM Omnibus Regulation (Regulation (EU) 2025/2083), which entered into force on 20 October 2025. The aim was to cut administrative burden, particularly for smaller importers, without weakening the climate goal.

The headline changes are:

- A 50-tonne de minimis threshold: Importers whose total annual imports of covered goods stay below 50 tonnes (cumulative net mass) are exempt from CBAM obligations, including reporting, authorisation and certificates. This replaces the former €150 per consignment exemption. Hydrogen and electricity are excluded from this exemption and remain in scope at any volume. The Commission estimates the threshold exempts around 90% of importers while still covering about 99% of embedded emissions.

- Certificate sales delayed to 2027: The sale of CBAM certificates was postponed from January 2026 to 1 February 2027. There are no certificate purchases in 2026 itself, although 2026 imports still create a financial liability that is settled in 2027.

- A later annual deadline: The annual CBAM declaration and certificate surrender deadline moved to 30 September of the following year. The first declaration, covering 2026 imports, is due by 30 September 2027.

- A lower quarterly holding requirement: The quarterly requirement to hold certificates was reduced from 80% to 50% of embedded emissions, easing cash flow during the year.

These measures delay and lighten the compliance load, but they do not waive the 2026 obligations for importers above the threshold.

Legal responsibility for CBAM sits with the EU importer, or their indirect customs representative. They are the party that must hold authorised CBAM declarant status, report embedded emissions, and surrender certificates.

But the data that drives those obligations is generated upstream, in the supply chain. EU importers depend on their non-EU suppliers, including UK manufacturers and exporters, to provide accurate, verified emissions data calculated to the EU’s methodology. Where verified data is not available, importers must use default values, which are typically higher and increase the cost. That makes good supplier data a commercial issue, not just a compliance one.

So CBAM affects two groups at once: EU importers who carry the legal obligation, and the suppliers worldwide who need to provide the emissions data those importers rely on.

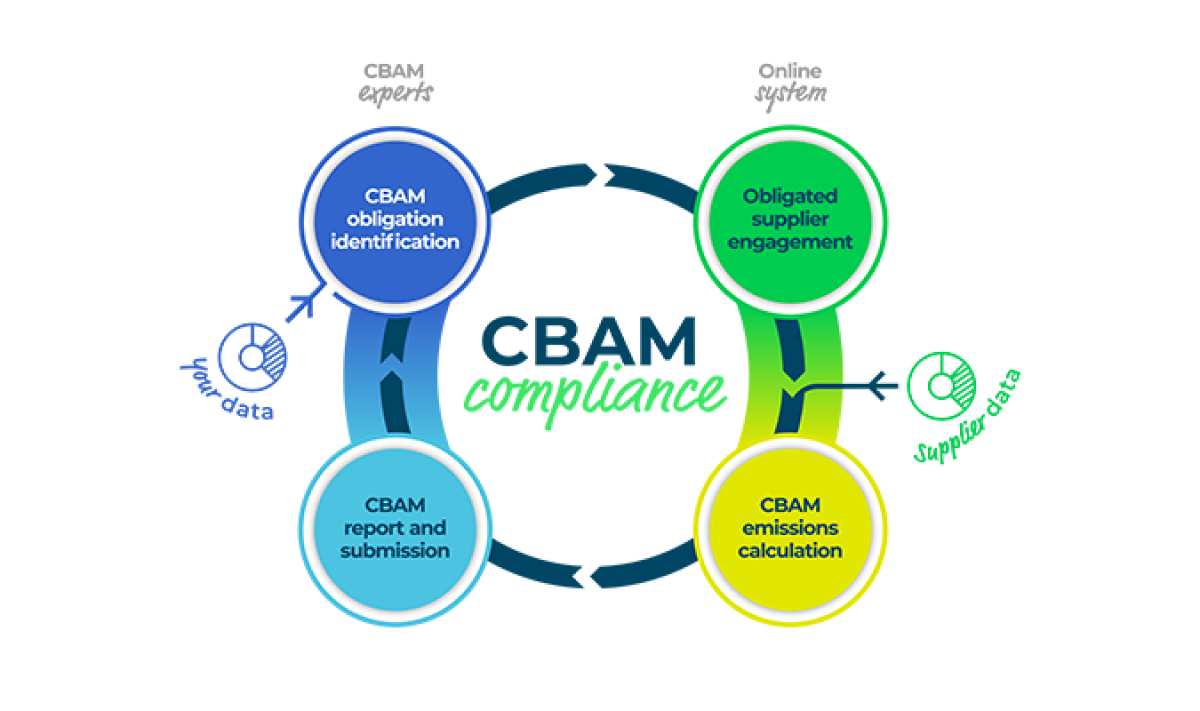

How CBAM compliance works

Under the definitive phase, three core obligations apply to EU importers above the 50-tonne threshold.

- First, they must hold authorised CBAM declarant status. Only authorised declarants may import covered goods above the threshold. Importers who submitted an application by 31 March 2026 can continue importing while their application is processed.

- Second, they must report embedded emissions. Each year, declarants file an annual declaration setting out the verified greenhouse gas emissions embedded in their imports. Where actual emissions data is used, it must be verified by an accredited third-party verifier. Where reliable data is unavailable, default values apply.

- Third, they must buy and surrender CBAM certificates to cover those emissions. A CBAM certificate represents one tonne of embedded CO2 emissions, priced on the EU ETS allowance price. Certificates are bought from national authorities, and the right number must be surrendered against the declared emissions each year.

If a carbon price has already been paid in the country where the goods were produced, that amount can be deducted, provided it can be evidenced.

Related regulations and resources

UK CBAM: a seperate scheme from 2027

The UK is introducing its own Carbon Border Adjustment Mechanism, separate from the EU’s. The UK CBAM is due to start on 1 January 2027, with the enabling legislation set out in the Finance Bill 2025 to 2026.

The UK scheme will cover a similar set of carbon-intensive goods, including iron and steel, aluminium, cement, fertilisers and hydrogen. Following consultation, the inclusion of indirect emissions has been proposed for delay until 2029 at the earliest, and the registration threshold has been revisited.

There is also movement on linking the two systems. The EU and UK have agreed to negotiate on linking their emissions trading schemes, which could eventually allow mutual exemptions between the EU and UK CBAMs. Until any such arrangement is finalised, UK businesses should plan for both regimes: supporting EU customers under the EU CBAM, and preparing for their own obligations under the UK CBAM from 2027.

How to prepare your business for CBAM

CBAM readiness is best treated as an operating capability rather than a one-off project. A practical starting point is to:

- Confirm your scope. Check whether your imports, or the goods you supply, fall under CBAM’s covered sectors.

- Assess your volumes. Work out whether you sit below or above the 50-tonne threshold, and whether you might cross it in a future year.

- Establish emissions data. Put in place the monitoring and supplier engagement needed to produce verified, methodology-aligned emissions data, rather than relying on higher default values.

- Plan for the cost. Even though certificates are not purchased until 2027, build the financial provision for 2026 imports into your planning now.

- Assign ownership. Make clear who is accountable for CBAM, since legal responsibility cannot be passed to a representative even where filing is delegated.

Acting early reduces the risk of customs disruption, higher default-value costs and last-minute pressure on verification capacity.

How Reconomy helps

CBAM sits within wider environmental compliance, where reliable data and clear processes matter most. Reconomy’s Comply Loop brings together compliance expertise from across our specialist brands to turn CBAM obligations into workable systems, from scope and supplier engagement to the verified emissions data your EU customers need, alongside preparing for UK CBAM from 2027.

Speak to our Comply team to understand your exposure and get the right processes in place.

Let’s close the circularity gap

The global economy is currently only 6.9% circular, which means over 90% of natural resources are being wasted rather than reused, repaired, or repurposed. This is not only unsustainable, but also unacceptable.

By continuing to do what we do, we’re helping to protect the global ecosystem and close the circularity gap. Through our #CloseTheGap movement, we’re turning circularity from a buzzword into a business advantage.

Frequently asked questions

CBAM, the Carbon Border Adjustment Mechanism, is an EU regulation that places a carbon price on imports of certain carbon-intensive goods, such as steel, aluminium, cement and fertilisers. It is designed to prevent carbon leakage by making imports carry a carbon cost similar to the one EU producers pay under the EU Emissions Trading System. Its definitive, financially binding phase began on 1 January 2026.

At the start of its definitive phase, CBAM covers imports of iron and steel, aluminium, cement, fertilisers, hydrogen and electricity, together with selected precursors. These sectors are carbon-intensive and at high risk of carbon leakage. In December 2025 the European Commission proposed extending CBAM to a range of downstream steel and aluminium goods from 2028, but that extension is still under negotiation and not yet law.

CBAM began with a transitional phase on 1 October 2023, which required quarterly emissions reporting but no payments. The definitive phase started on 1 January 2026, when EU importers above the threshold became financially liable for the emissions embedded in their imports. CBAM certificate sales begin on 1 February 2027, and the first annual declaration, covering 2026 imports, is due by 30 September 2027.

Legal responsibility for CBAM rests with the EU importer, or their indirect customs representative, who must hold authorised declarant status, report embedded emissions and surrender certificates. However, the emissions data comes from suppliers upstream, so non-EU manufacturers and exporters, including UK businesses, are also affected. They need to provide verified emissions data so their EU customers can report accurately and avoid higher default-value costs.

A CBAM certificate represents one tonne of CO2 emissions embedded in imported goods. Authorised CBAM declarants buy certificates from national authorities and surrender enough to match the verified emissions in their imports each year. The certificate price is linked to the EU Emissions Trading System allowance price. Certificate sales begin on 1 February 2027, with no purchases required during 2026.

Yes. Under the 2025 simplifications, importers whose total annual imports of covered goods stay below 50 tonnes (cumulative net mass) are exempt from CBAM obligations, including reporting, authorisation and certificates. This single mass-based threshold replaced the former €150 per consignment exemption. Hydrogen and electricity are excluded from the exemption and remain in scope at any volume.

Yes. The UK is introducing its own Carbon Border Adjustment Mechanism, separate from the EU’s, due to start on 1 January 2027 under the Finance Bill 2025 to 2026. It will cover similar goods, including iron and steel, aluminium, cement, fertilisers and hydrogen. The EU and UK are also negotiating on linking their emissions trading schemes, which could allow mutual CBAM exemptions in future.

UK exporters of CBAM goods should review which of their products fall in scope, then put in place the monitoring needed to provide verified emissions data to their EU customers, since EU importers depend on that data to report accurately. Engaging early helps customers avoid higher default-value costs. UK businesses should also prepare for the separate UK CBAM, which starts in 2027.

Speak to our CBAM experts